It’s a situation that almost every small-business owner knows: You did the work, you sent the invoice, and – nothing. The days turn into months, your emails go unanswered, and the client has disappeared into the ether with your hard-earned money.

For small-business owners, late payments aren’t just emotionally draining – they can be financially ruinous. Australian Small Business and Family Enterprise Ombudsman (ASBFEO) Bruce Billson states that late and unpaid invoices are among the biggest challenges SMEs face today. His office exists to advocate for small businesses and provide resources to help them navigate issues like payment disputes.

“The main [reason] is largely just how challenging the business environment is, and that there’s margin squeeze happening across the small-business economy,” Bruce says.

“More than two-in-five cases we help with now involve a payment dispute. [Before Covid-19], we’re talking about less than one-in-four. It’s been a substantial uptick.”

“I feel like it’s almost a rite of passage to have had a non-payer,” says Jasmine Parasram, a sole trader of 15 years who owns two small businesses: Jasmine Designs and Creative Business Kitchen. Jasmine has dealt with so many of these situations over the years that she now helps other business owners navigate them under the moniker of “the Pricing Queen”.

“The average freelancer has $20K worth of unpaid invoices in their inbox,” Jasmine explains. “But it gets less and less common the more you learn the lessons.”

If you’re facing payment problems, you’re not alone – and this article is for you. It will explore, in simple terms, what your options are when chasing up elusive payments. We’ll go over why payment disputes happen, how to prevent them from happening, and what to do if you end up in a situation where someone isn’t accepting the bill.

Why payment issues happen

As Jasmine explains, it’s common for business owners to blame themselves for payment mishaps.

“The guilt and the shame that comes from it is massive,” she explains. “The freelancers often blame themselves, because there are things that they could have done, like withholding deliverables until the whole amount is paid, or being brave enough to speak up and call out bad behaviour.”

But non-payment isn’t a ‘you’ problem. You’ll be unsurprised to find out that the most common cause is financial difficulty, the ASBFEO states. It’s not just the high cost of living, either. With the ATO now cracking down on small-business debt, many are prioritising these repayments over paying larger businesses. In other words, if someone isn’t paying you, it’s most likely because they simply can’t afford to do it.

With that in mind, it’s important to be careful about how we view payment disputes, Jasmine says.

“Everyone seems to take payments personally,” she says. “It’s not a personal vendetta. It’s not against you, it’s not an emotional thing.”

How do you prevent payment problems?

Nobody wants to have to chase up payments, so how do you prevent payment pickles in the first place?

It starts with avoiding clients who are likely to cause issues, both of our contributors argue. If your potential client is another business, Bruce says that you may want to check with a credit reference bureau, such as CreditorWatch, to understand their current financial situation. If the business has a few outstanding debts, especially to the ATO, engaging with them is probably a bad idea.

When it comes to the sort of problems you’ll run into with large businesses, Bruce explains that changing payment terms are usually the issue.

“The larger [companies] tend to just change the payment terms unilaterally, and a small business supplier’s sort of stuck with it, particularly where they’re so dependent on that relationship,” he says.

The government has introduced a payment times reporting register to help keep large businesses accountable. Unfortunately, Bruce says, this is often complicated to use, so it’s not easy to get quick information as an SME supplier about who is honouring payments and who is not.

In Jasmine’s experience, one of the biggest mistakes you can make is not following your gut feeling when meeting potential new clients.

“Some clients, you can tell they’re going to be shitty payers,” she says.

You also might need to be wary of more than just payment times. Even if a client has the funds to pay on time, you can lose your valuable time to nitpickers, hagglers and those who don’t appreciate your value.

“I’ve turned clients away at the beginning,” Jasmine says. “It hasn’t necessarily been because I think they’re going to be bad payers. It’s the ones who control the creative process, the ones you haggle over the price, the ones that suggest you take shortcuts.”

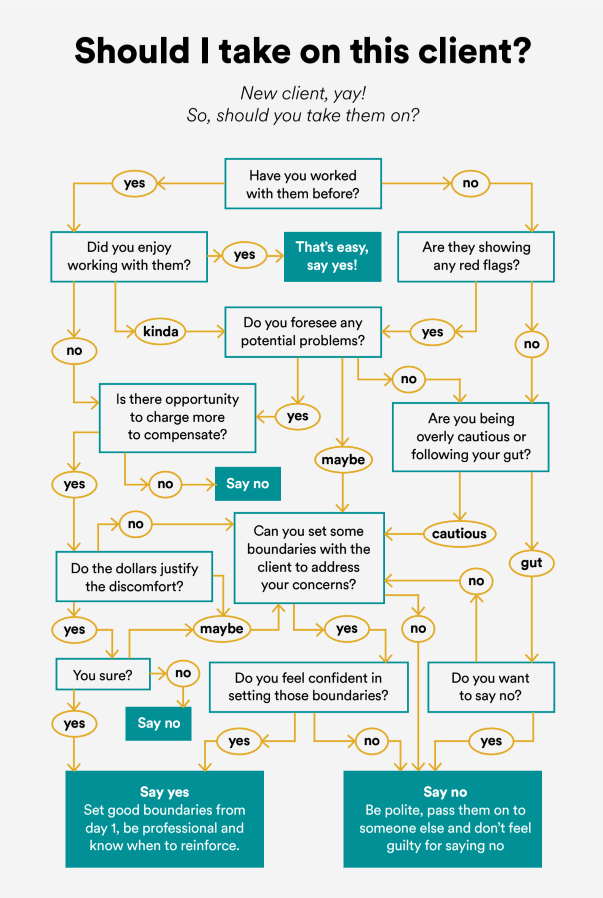

To make the process of deciding whether to take on a client easier, Jasmine created a quick-reference “client contemplation” flowchart for her Creative Business Kitchen community:

Preventing payment issues after you’ve taken on a client

Aside from simply not getting involved with the wrong people, there are some other steps you can take to prevent a mishap from occurring after you’ve taken on a new client.

The first, and most obvious, is to have a watertight contract ready. An excellent contract will “show the battle scars” that an experienced small-business owner has obtained over the years, Jasmine explains.

Crucially, it should involve a process for collecting payments in case of difficulties, both Jasmine and Bruce say. For instance, you might add a percentage to the bill for every week of non-payment, to cover the time spent chasing after the money. You may want to cap this interest up to a certain sum, but it’s a good way to cover yourself in case of a payment pickle.

If anything goes awry, you can refer back to your contract. It takes some time and emotion out of advocating for yourself, because, as Jasmine points out, the client has already agreed to respect your time and money.

“[The client] agreed that if they don’t pay extra, the next steps in the process are the responsibility of both you and them to navigate,” Jasmine points out.

Another way to protect yourself: Always delay key deliverables until you actually get paid.

“More often than not, people are in a position where they feel uncomfortable about charging, especially as a freelancer, so they avoid it by starting to do the work because they’re so excited, or delivering everything before they get paid,” Jasmine explains.

Finally, consider setting up a direct-debit system when collecting payments. That way, money comes straight out of your client’s account when it’s payment time.

“I personally use GoCardless, where it just automatically charges them and then gets that payment from them,” Jasmine says.

What to do if someone isn’t paying

Let’s say you did your due diligence on a client, your gut feeling was good, but now there’s a payment problem. It happens. What do you do?

“The advice that we provide is to make sure the party that owes you the money is aware that you are owed the money,” Bruce says. “Just: ‘How are you going? Just a quick call, I noticed that payment that was due today hasn’t come in. Have you got all the information you need? Is the invoice what you expected?’

The ASBFEO has found a rise in cyber scams involving invoice substitution, where a criminal changes your bank details on an invoice to redirect payment elsewhere. This can be something to watch for – or a pretext to check in with your client while showing helpfulness and concern, Ombudsman Bruce points out.

“Even confirming that [the invoice] has landed with the right people and that your account details are accurate – that’s a good early call,” he says.

If you’re uncomfortable about going after what you’re owed, you’re most definitely not alone. Being uncomfortable asking for money is a common problem among business owners, Jasmine says.

“They feel very uncomfortable about it when they put it as ‘asking for money’. I put it as ‘letting people know the bill’,” she says. “You wouldn’t expect to eat an entire meal at a restaurant and walk out the door without paying. So the same thing is true when you are running a business.”

When you are ‘collecting the bill’, it’s always useful to make the process less personal; Bruce and Jasmine suggest setting up automations around payment, like invoicing services that send the bill to your client’s inbox automatically.

“Remove the emotion,” Jasmine advises. “They’re not emotional about the money, neither should you be.”

What if a client says they can’t pay you?

If someone can’t pay you, a good first step is to ask for a portion of the money – or put them on a formal payment plan.

“You might say, ‘Look, can I get some of it in the bank? Because I’ve got my bills to pay as well. And if you’re in a tight spot now, is there some portion of it you can pay now?’ ” Bruce says. “And then you can talk about a payment plan or something like that.”

This step is about levelling with the person and keeping everyone’s dignity intact. The Ombudsman points out that you don’t want to burn any important business relationships unless you really have to do that.

“If you get to the point where you think nothing’s changing and you’re doubting whether there’s a genuine interest, it may be time to issue a letter of demand – a more formal notification that you’re owed money,” he adds. “And we provide some resources to help people do that, because often it’s the first time they’ve had to chase up and they’re not quite sure what their moves are.”

Business.gov has a useful resource page for writing a letter of demand, including a template you can base yours off.

If a letter of demand doesn’t work, you might want to bring in a third-party resolution service. The ASBFEO website also has a resource for finding the right service for you – see https://asbfeo.gov.au/disputes-assistance/dispute-support. The online tool asks you a number of questions about your issue, location and business, to point you towards the body that can best help you. It also provides a range of ways you can contact each body.

You do have legal and consumer law obligations when contacting other businesses about debt; read the debt collection information on the Australian Competition & Consumer Commission (ACCC) website.

You can also contact a debt-collection agency to help you recover expenses; it may be best to inform your customer that you plan to use one. If you’re going down this road, the ACCC has put together some debt collection guidelines for collectors and creditors.

If the dispute is heating up, but you don’t wish to go to court, you may consider alternative dispute resolution, such as mediation. ADR’s benefits include lower costs, quicker timeframes, confidentiality, and a more flexible and collaborative dispute resolution process. Once again, the ASBFEO has a resource for finding an ADR practitioner in your state who can help you, or you can search the Mediator Standards Board website to find a nationally accredited mediator.

You can also lodge a complaint through your state or territory’s Fair Trading agency, which can act as an informal negotiator.

Taking the matter to court should be your last option, the ASBFEO warns. While some small-business owners manage to resolve issues in a small claims court, the process is usually expensive and time consuming.

Further resources

- The ASBFEO offers a range of dispute support services.

- Business.gov.au offers a range of resources and guides on payment issues. See: ‘What to do when you haven’t been paid’ and ‘Resolve disputes’ pages.

- See the ACCC’s debt collection guidelines if you’re thinking of using a debt-collection agency.

- If you need mental health support, NASBO (NewAccess for Small Business Owners) is a guided self-help mental health program that aims to support you in overcoming a particular program, such as a payment dispute.

- Call the free small business debt helpline on 1800 413 828 if you’re in financial difficulty.

- The Small Business Mentoring Service provides low-cost mentoring in all areas of running a business.